A credit union membership offers you many ways to save, but did you know there’s an easy way to help your savings grow even more over time? And best of all—you don’t need to do anything other than choose the right type of account and make your initial deposit. It’s called compound interest. Credit unions pay "dividends" on shares, such as savings or certificates, in your account. Credit union dividends compound the same way interest compounds.

What is compound interest?

Your deposits into savings, money market, and certificate accounts earn interest; that interest is calculated as a percentage of the amount in your account. The interest you earn along the way is typically added to your account balance, and over time, this allows your balance to grow.

When interest is compounded, it means the interest you’ve earned along the way is earning interest itself. In other words, you’re earning interest both on your original deposit, as well as on the interest you’ve earned over time. And, like a snowball that grows bigger as it rolls down the hill, compounding causes your account balance to grow exponentially over time.

How does compound interest work?

The amount you earn in compound interest is determined by how much you have saved (your principal), your rate of return (the interest rate), and the way in which the interest compounds. Compounding can occur daily, weekly, monthly, quarterly, or annually. Interest that is compounded more frequently helps your savings grow more quickly.

For example, if your account compounds daily and earns 4% interest, you earn 1/365th of the 4% each day. But since your balance increases a little bit every time you earn interest, which is every day with daily compounding, the amount you earn with interest increases every day as well.

Time is another important factor in how compound interest works. The longer your money sits in savings, the more time it has to grow. And because that growth happens exponentially, you’ll earn increasingly more over time. As you earn interest and that interest is added to your account balance, you have a larger balance, which earns even more interest.

Simple versus compound interest

There are two common ways to calculate interest.

- Simple interest is calculated only on the amount of the initial balance. This growth is a straight line.

- Compound interest is calculated on both the initial balance and any interest you earn along the way. This means your interest earns interest of its own, and your balance gets bigger over time as it grows exponentially.

And the beauty is that you don’t need to do anything other than sit back and watch your money grow.

What makes compound interest so… interesting?

At first glance, it might not seem like a big deal. But over time, the benefits of compound interest can really add up. Let’s compare the earnings of a certificate account that earns compounded interest with one that just earns simple interest. We’ll also see how time and the rate of compounding makes a difference.

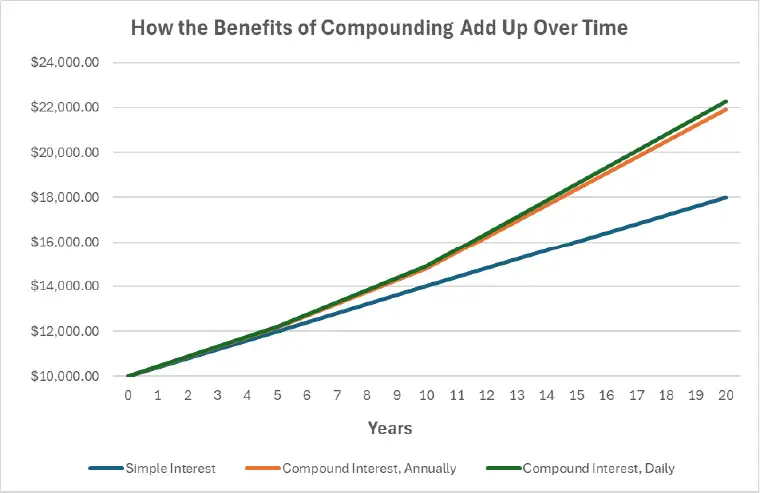

Say you have a $10,000 initial deposit, with no additional deposits made along the way, in an account earning 4% interest with no rate variance during the period.

After 5 years, your balance will be:

- Simple interest:* $12,000.00

- Compound interest, compounded annually: $12,166.53

- Compound interest, compounded daily: $12,213.89

Over time, the difference between the three becomes even bigger.

Here’s your savings balance after 10 years:

- Simple interest: $14,000.00

- Compound interest, compounded annually: $14,802.44

- Compound interest, compounded daily: $14,917.92

And after 20 years:

- Simple interest: $18,000.00

- Compound interest, compounded annually: $21,911.23

- Compound interest, compounded daily: $22,254.43

Calculations: Compound Interest Calculator | Investor.gov

*Simple interest is the interest that is only calculated on the initial sum. In the first example, this is calculated as 10,000x.04 = $400 interest per year, or $2000 every 5 years.

Compounding also applies to interest you pay for debt owed

While compound interest benefits you when you save, it can also challenge you if you owe money on things like credit card balances, car loans, or a mortgage. All of these types of loans charge compounded interest.

For example, when you pay your entire credit card balance each month, you avoid having to pay interest. But if you do not pay the entire amount due each month, that balance is subject to interest owed. Most credit card companies compound the interest you pay on credit card balances, which means that over time, you could end up owing more and more if you don’t make more than the minimum monthly payment.

Put the power of compound interest to work for you

Here’s how to take full advantage of the benefits of compound interest:

- Choose a savings option that offers compound interest.

- If possible, choose one that compounds daily. Over time, this adds more to your balance.

- Start saving as early as possible; this gives the compound interest you earn more time to grow.

- Be consistent and make contributions to your savings over time. Even small amounts add up, particularly with compounding.

For example, when you open a Certificate account at Global Credit Union with a term of 12 months or more, choose to have your dividends automatically reinvested back into the certificate, or have the money automatically reinvested in another share or account at Global. You can change these options at any time during your certificate term.

Compound interest lets the money you earn from interest earn interest itself. It’s an easy way to boost your savings, and it doesn’t cost you anything. The best way to take advantage of compounding is to begin saving early. Then sit back and let compounding work its magic.